More Listings and Lower Rates

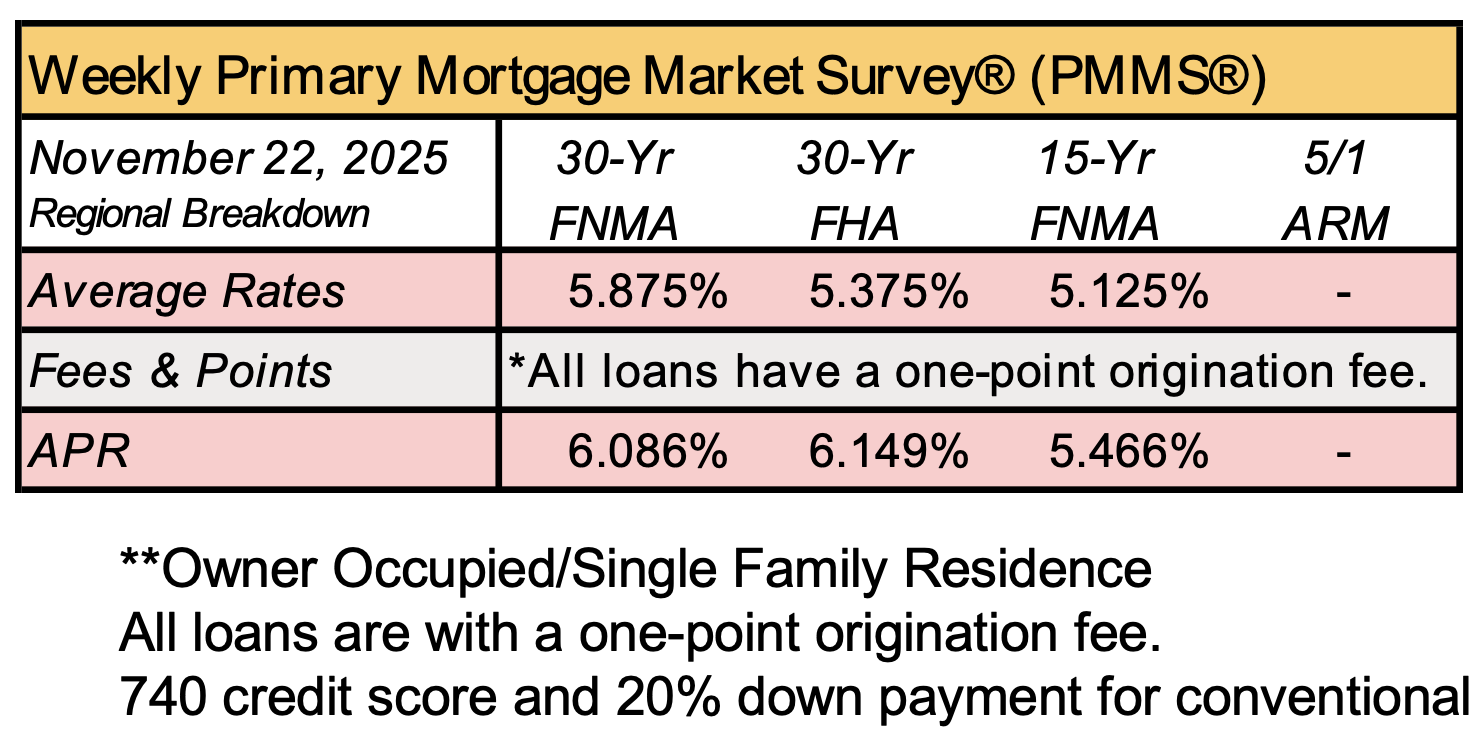

Mortgage interest rates continued to trend lower in October, ending the month at 6.17% for 30-year fixed-rate loans, the lowest level since early October 2024. Across NWMLS counties, the number of sales and median prices fell year-over-year by 4% and 1.5%, respectively, while active listings jumped 27%, giving buyers more options in the market despite ongoing affordability challenges.

Compared to September, both sales and median prices increased modestly, by about 1% and 1.5%, following declines in the previous month.

“The year-over-year numbers suggest that potential buyers continue to be constrained by high interest rates. While it might be tempting, it would be overreaching to attribute the latest month-over-month changes to lower interest rates. One month of data does not constitute a trend, and it is very difficult to predict whether the current moderating trend will continue,” said Steven Bourassa, Director of the Washington Center for Real Estate Research at the University of Washington. -MLS

Source: NWMLS

What is a 50-year mortgage? The pro and cons of Trump’s proposal

Recently, President Donald Trump stirred the housing world by posting an image comparing the classic 30-year mortgage (a legacy of FDR) to his proposal of a 50-year mortgage. According to reports, the Federal Housing Finance Agency (FHFA) is “working on the 50-year mortgage” in response to housing-affordability pressures.

What is a 50-year mortgage?

Simply put, it’s a home loan stretched over five decades instead of 30 years, reducing monthly payments by spreading principal and interest over more time. Most U.S. mortgages are capped at 30 years under Qualified Mortgage (QM) rules from the Dodd-Frank Act. Expanding to 50-year terms would likely require regulatory changes or creative loan classifications.

The Pros: Why buy-side consumers might consider:

Lower monthly payments: Stretching a loan from 30 to 50 years lowers monthly payments, helping buyers qualify for larger homes or compete in high-cost markets.

Greater access to homeownership: For buyers squeezed by income or limited down payments, a longer amortization could open doors that might otherwise stay closed.

More flexibility in cash flow: Smaller payments can free up funds.

For maintenance, savings or emergencies-offering breathing room early on.

-Read more inman.com

Seattle homebuyers are less likely to back out of deals

Across the country, more homebuyers are walking away from purchase contracts, but in Seattle, most are staying the course.

In August, 15.1% of national real estate details fell through, marking the highest share since 2017. By contrast, the Seattle metro area saw a modest uptick from 9.7% to 10%, keeping local buyers among the least likely to renege on their contracts.

The reasons vary. During the pandemic-era seller’s market, buyers often waived contingencies, leaving little room to withdraw from deals.

In Seattle, however, two factors are helping keep deals intact: financial stability and limited supply. Low inventory also plays a role.

-getthewreport.com

Gina Brown (NMLS# 115337)

Senior Loan Officer

🏢 C2 Financial (NMLS# 135622)

425-766-5408

ginabrown@C2financial.com

www.loansbygina.com