Dog days of August cool sales but expand opportunities for buyers

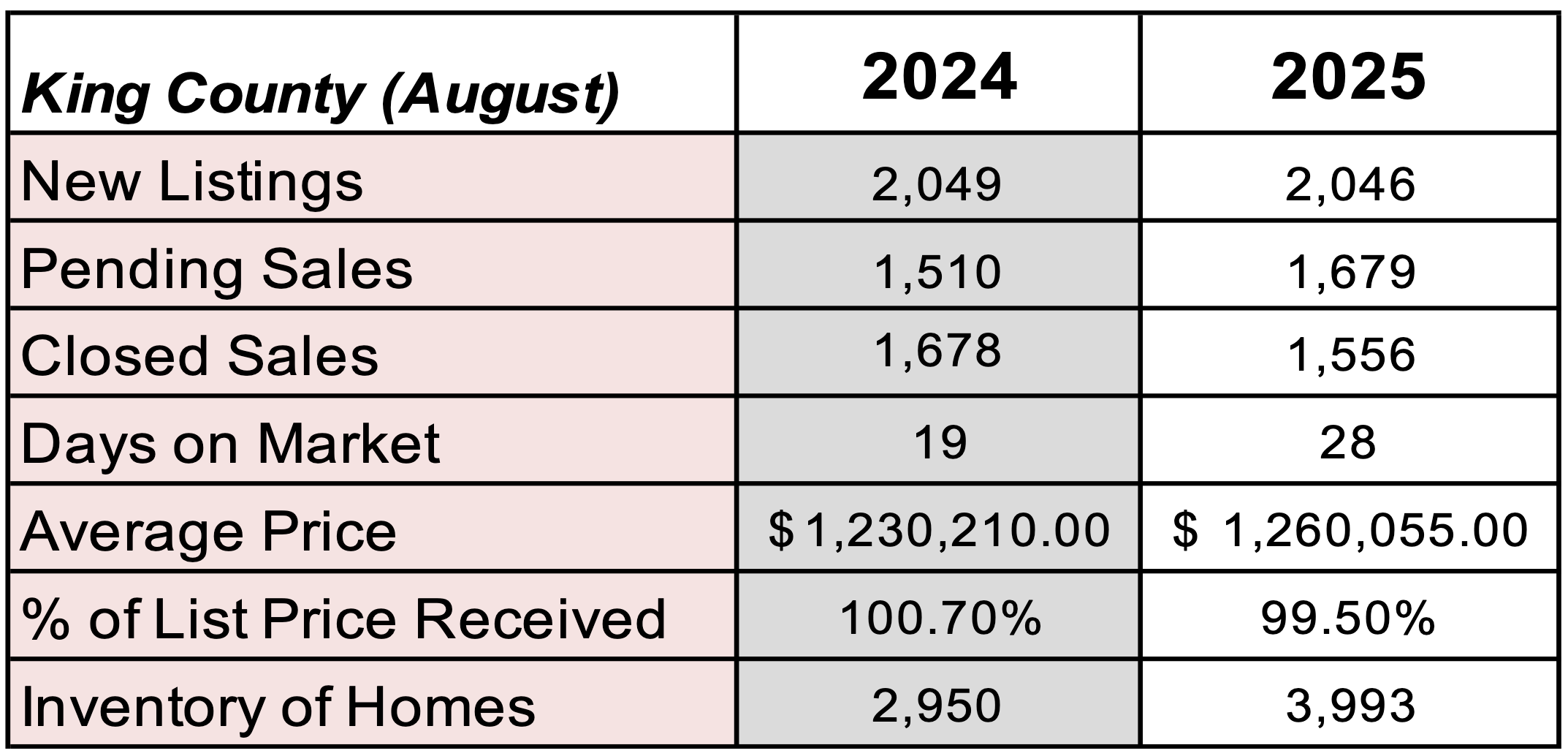

In August, both active listings and home sales declined compared to July—by 2.7% and 7.7%, respectively—across the 27 counties in the NWMLS coverage area. This slowdown was largely driven by weaker activity in King and Snohomish counties. Compared to the same time last year, listings rose by 30.8%, but sales fell by 5.7%, indicating continued stagnant buyer demand. Median home prices remained flat month-over-month and increased just .8% year-over-year.

Active Listings

There was a 30.8% increase in total number of properties listed for sale year-over-year, with 20,219 active listings on the market at the end of August 2025, compared to 15,453 at the end of August 2024. When compared to the previous month, active inventory decreased by 562 listings (-2.7%), down from 20,781 in July 2025.

The number of homes for sale year-over-year increased throughout the NWMLS coverage area, with 25 out of 27 counties seeing a double-digit year-over-year increase. The six counties with highest year-over-year increases in active inventory for sale were Ferry (+63%), Snohomish (+50.1%), Jefferson (+47.3%), Clallam (+46.3%), Columbia (+45.8%), and Thurston (+38.9%).

Source: NWMLS

Mortgage Rates HIGHER (Not Lower) After Fed Rate Cut

Several things happen on Fed Day–especially on the 4 out of 8 examples with updated rate forecasts from Fed members. The official announcement of a rate cut is typically the least important aspect. In fact, it is usually entirely unimportant in terms of its impact on mortgage rates.

Instead, the bonds that determine mortgage rates are much more likely to react to the Fed’s dot plot (the chart showing each Fed member’s rate forecast over the next few years) and the press conference with the Fed Chair.

The dots are released at 2pm at the same time as the rate cut announcement. The press conference follows at 2:30pm and usually lasts 50 minutes. This staggered timing makes for plenty of back and forth volatility on occasion and today was a prime example.

The dots helped bonds because they signaled better odds for two additional cuts in 2025 as opposed to only one. The market was mostly expecting that, but it wasn’t fully priced-in to prevailing rates. Things changed during Powell’s press conference and bonds ended up more than reversing the initial move.

Powell framed today’s cut as a “risk management” cut and emphasized that the forecasts in the dot plot do not represent a plan for future cuts. Rather, the Fed will continue to take things on a meeting by meeting basis and make decisions based on the new data that becomes available over that time.

As the underlying bond market responded, most mortgage lenders issued mid-day changes to the rates announced this morning. The net effect is that mortgage rates are most certainly HIGHER this afternoon compared to yesterday’s latest levels, not to mention this morning’s.

-Matthew Graham (Mortgage News Daily)

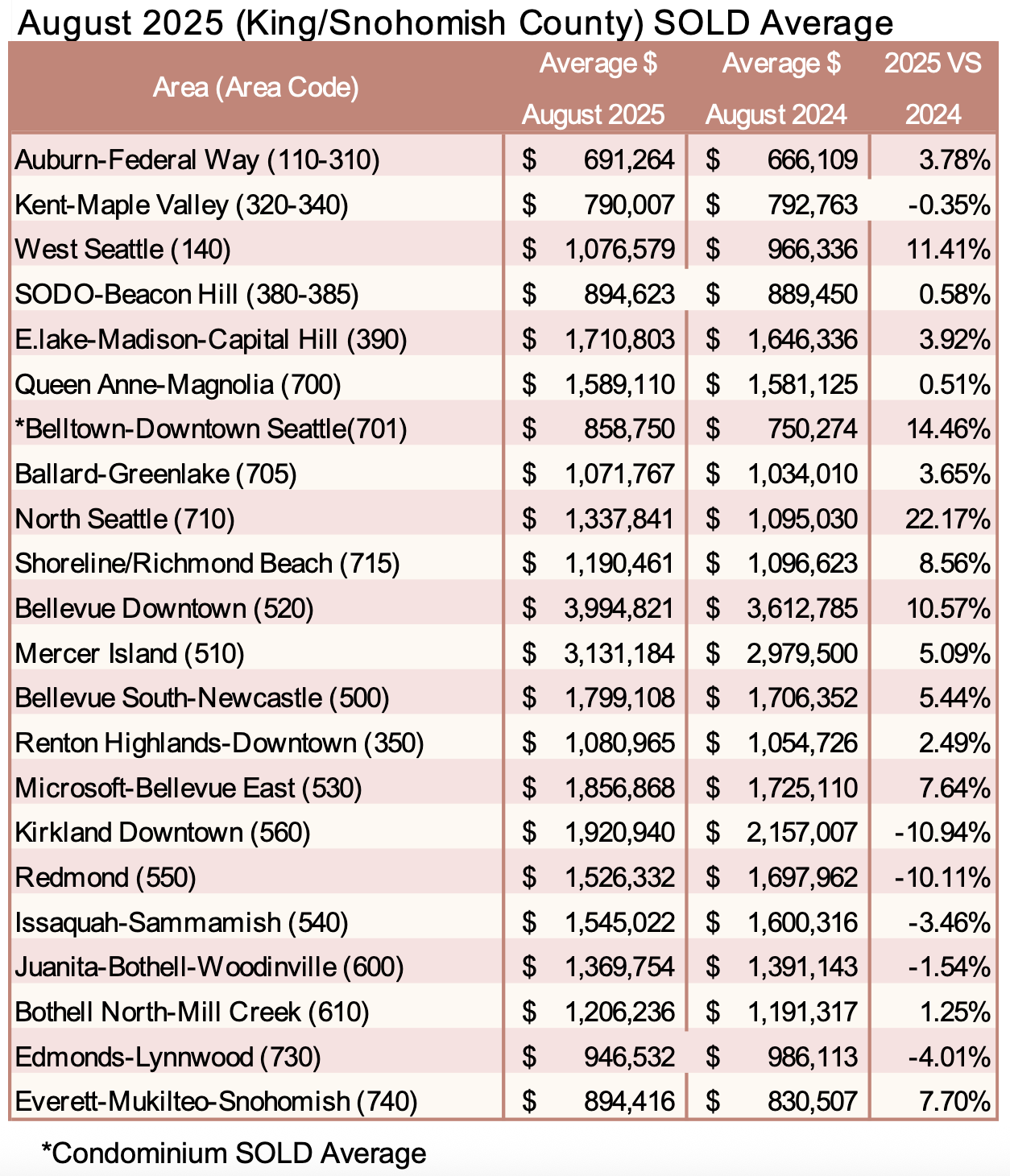

Breakouts! – Residential SOLD Average

Fed Cuts Interest Rate: What Happens to Mortgage Rates Now as Markets React

The Federal Reserve has lowered its benchmark interest rate by a quarter percentage point, in a highly anticipated decision surrounded by extraordinary political drama.

The 11-1 decision supported by Fed Chair Jerome Powell and a majority of the Federal Open Market Committee (FOMC) brings the central bank’s overnight rate down to a range of 4% to 4.25%, marking the first change in rate policy in nine months.

President Donald Trump‘s economic adviser Stephen Miran, newly appointed to the Fed’s Board of Governors and sworn in on Tuesday, was the lone dissenting vote on the panel, calling instead for a larger half-point rate cut.

In a press conference following the decision, Powell called the rate reduction a “risk management cut” in response to rising unemployment, pointing out that inflation remains elevated.

“We have a situation where we have two-sided risk, and that means there’s no risk-free path,” said Powell, referring to the dual threats of inflation and rising layoffs. “And so it’s quite a difficult situation for policymakers.”

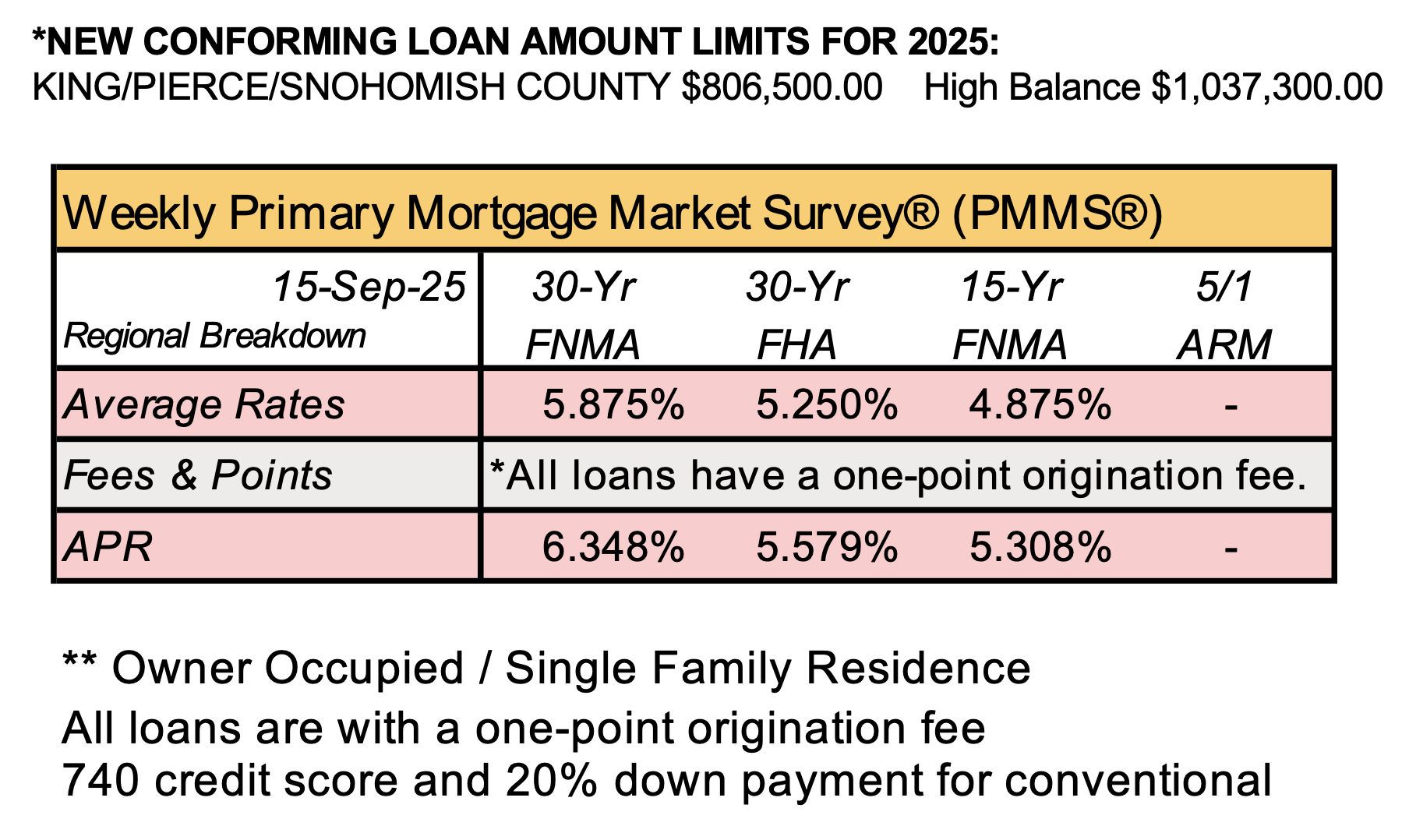

A quarter-point cut was widely anticipated and already largely priced into mortgage rates, which have fallen in recent weeks and reached an 11-month low of 6.35% last week, according to Freddie Mac.

Mortgage rates typically follow long-term bond yields, which moved higher on Wednesday as markets digested the summary of economic projections issued by the FOMC alongside the rate decision.

Those projections showed Fed policymakers have a median expectation of making two additional rate cuts this year, but just one in 2026—fewer than the three cuts next year that markets had anticipated.

“This ongoing gap between market and Fed expectations means that some risk of upward pressure on mortgage rates remains,” says Realtor.com® Chief Economist Danielle Hale. “But for now, consumers have already benefited from the drop in mortgage rates that has brought mortgage rates below 6.5% for the first time in nearly a year and is likely to continue at least through this week.” -Keith Griffith (Realtor.com)

Gina Brown (NMLS# 115337)

Senior Loan Officer

🏢 C2 Financial (NMLS# 135622)

425-766-5408

ginabrown@C2financial.com

www.loansbygina.com